Understanding the Differences Between Term and Whole Life Insurance

What Is Life Insurance?

Life insurance serves as a financial safety net for families and dependents. It provides a lump sum payment when the insured person passes away. This payment can help cover daily living expenses, funeral costs, and outstanding debts. The primary goal is to ensure that your loved ones are not left in financial distress after your departure.

There are several types of life insurance available, each designed to meet different needs and preferences. Understanding these options can help individuals make informed decisions about their financial planning.

What Is Term Life Insurance?

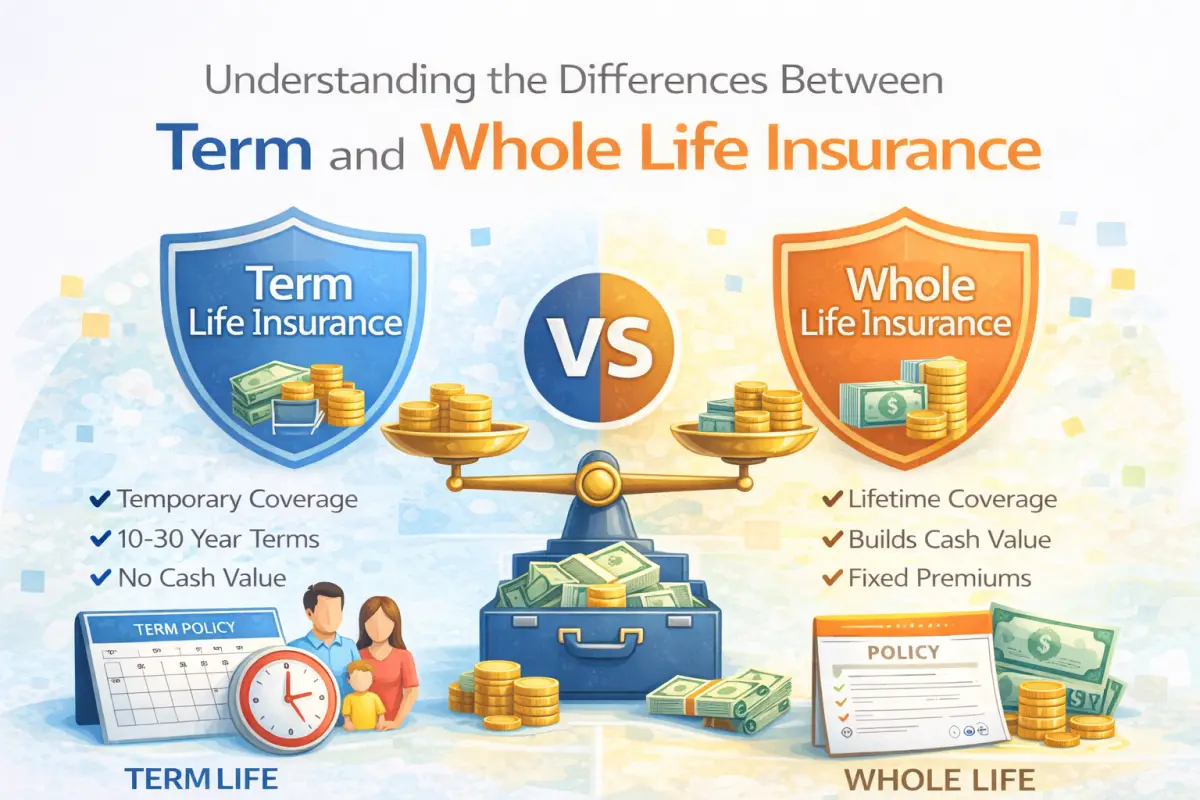

Term life insurance is a straightforward type of coverage. It is purchased for a specific period, often ranging from 10 to 30 years. If the insured dies within this timeframe, the beneficiaries receive a death benefit. If the term expires and the insured is still alive, the coverage ends without any payout.

This type of insurance is often chosen for its affordability. The premiums are generally lower compared to whole life insurance, making it an appealing option for those seeking budget-friendly coverage. However, it does not accumulate any cash value over time.

What Is Whole Life Insurance?

Whole life insurance, on the other hand, provides coverage for the entire lifetime of the insured, as long as premiums are paid. Unlike term insurance, whole life policies build cash value, which grows at a guaranteed rate. This can be used as a savings component, allowing policyholders to borrow against the policy or withdraw funds if needed.

The premiums for whole life insurance are higher than those for term policies. However, they provide lifelong coverage and the potential for cash accumulation, which can be beneficial in financial planning.

Term Life vs Whole Life Insurance: Side-by-Side Comparison

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Duration | Fixed term (e.g., 10, 20, or 30 years) | Lifetime coverage |

| Premiums | Generally lower | Higher premiums |

| Cash Value | No cash value | Builds cash value |

| Policy Loans | No loans available | Loans can be taken against cash value |

| Best For | Short-term needs | Long-term financial planning |

Cost Differences: Term vs Whole Life Insurance

The costs associated with term life insurance are typically much lower than those of whole life policies. This difference is due to the fact that term insurance only pays out if the insured dies within the term. Whole life insurance, being a lifelong commitment, incurs higher premiums due to the guaranteed payout and cash value accumulation.

For individuals looking to minimize expenses while securing coverage, term life may be the more suitable option. On the other hand, those seeking to invest in a long-term financial product may find whole life insurance more beneficial despite the higher costs.

Cash Value Explained (Whole Life Insurance)

The cash value aspect of whole life insurance is a key feature. It allows policyholders to accumulate savings over time. A portion of each premium payment contributes to this cash value, which grows tax-deferred. Policyholders can access this money through loans or withdrawals, providing flexibility in financial management.

This feature can serve various purposes, such as funding education, supplementing retirement income, or covering emergencies. However, loans taken against the cash value may reduce the death benefit if not repaid.

Which One Is Better for Families?

For families, the choice between term and whole life insurance depends on their financial situation and goals. Term life insurance is often more suitable for young families needing affordable protection to cover essential expenses like mortgage payments and childcare. It provides a financial cushion during critical years.

Whole life insurance, while more expensive, can be beneficial for families looking to establish a long-term financial strategy. Its cash value can serve as a source of funds during emergencies or future financial needs.

Which One Is Better for High-Income Earners?

High-income earners may find whole life insurance attractive due to its cash value and tax advantages. The ability to borrow against the policy can provide liquidity and financial flexibility. Additionally, whole life insurance can be an effective estate planning tool, helping to transfer wealth to heirs with minimal tax implications.

However, term life insurance can still play a role in a high-income earner's portfolio, especially if they seek to cover specific financial responsibilities that may diminish over time.

Flexibility and Policy Customization

Term life policies typically offer limited customization. They provide straightforward coverage for a set duration, which may not suit everyone. In contrast, whole life insurance allows for more flexibility. Policyholders can adjust their premiums and coverage amounts and take advantage of the cash value feature.

Customization options can be appealing for individuals looking to tailor their insurance to fit their unique financial needs and goals.

Tax Benefits Comparison

Both term and whole life insurance come with certain tax advantages. The death benefit from either policy is generally tax-free for beneficiaries. Whole life insurance also allows for tax-deferred growth of cash value, making it an attractive option for those interested in long-term savings.

In contrast, term life insurance does not accumulate cash value, which means it does not offer the same potential for tax-deferred growth. However, it can still provide essential financial protection without the burden of high premiums.

Common Myths About Term and Whole Life Insurance

Several misconceptions surround life insurance. One common myth is that whole life insurance is always a better option due to its cash value. However, this depends on individual needs and financial goals. Term life can be more suitable for those seeking pure protection without investment components.

Another myth is that life insurance is only necessary for those with dependents. Even single individuals may benefit from coverage, particularly if they have debts or wish to leave a legacy.

How to Choose Between Term and Whole Life Insurance

Choosing between term and whole life insurance requires careful consideration of various factors. First, assess your financial situation, including income, expenses, and long-term goals. Determine whether you need temporary coverage or a lifelong policy.

Next, consider your family’s needs and how life insurance can play a role in their financial future. Consult with a financial advisor to explore the benefits and drawbacks of each type of policy in relation to your specific circumstances.

Can You Have Both Term and Whole Life Insurance?

Yes, it is possible to have both term and whole life insurance. Many individuals choose to combine these policies to create a comprehensive coverage strategy. Term insurance can provide immediate protection for specific needs, while whole life insurance offers lifelong coverage and cash value accumulation.

This combination allows for flexibility and can help ensure that both short-term and long-term financial needs are met.

Expert Tips for Buying Life Insurance in 2026

As you consider life insurance options, keep a few tips in mind. First, shop around for quotes from different insurers to find the best rates. Use online comparison tools to evaluate various policies and coverage options.

Second, reassess your needs periodically. Life circumstances change, and so do insurance needs. Regularly reviewing your coverage can help ensure it continues to meet your goals.

Final Verdict: Term Life vs Whole Life Insurance

Both term and whole life insurance have unique advantages. Term life is typically more affordable and straightforward, making it suitable for those with temporary needs. Whole life insurance, with its lifelong coverage and cash value, is ideal for those seeking long-term financial planning.

Ultimately, the best choice depends on individual needs, financial situations, and future goals. By carefully considering these factors, you can make an informed decision that aligns with your financial strategy.